In step with the construction of the former article, this one is split into 3 views: visitor, app panorama, and generation. Every of those sections is additional subdivided to deal with explicit gaps. Determine 1 depicts this construction and summarizes the principle gaps recognized within the earlier article.

Determine 1: Views and gaps

Within the article, we wish to focal point on recommending movements that OEMs can take to near, or a minimum of slender, those essential gaps, drawing on insights from a contemporary international on-line survey of greater than 2,700 contributors from China, america, and the EU. This article is going to focal point on crucial of the ones gaps. Ideas for last the opposite gaps shall be put ahead in our impending Attached Automobile Pattern Radar record.

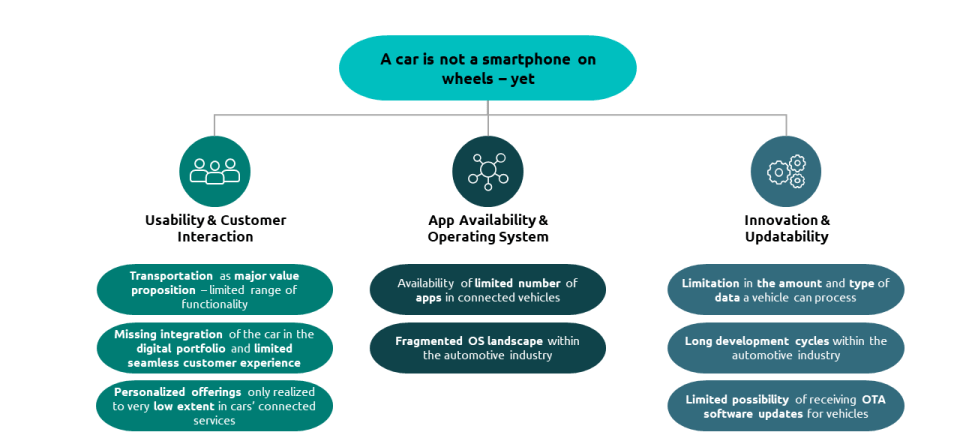

Buyer point of view: usability & visitor interplay

Price Proposition

Transportation continues to be the main price proposition for these days’s automobiles. This fairly slender focal point method there’s a hole between the variability of capability to be had to shoppers by the use of their automobiles and by the use of their smartphones.

Transportation is more likely to stay the automobile’s major price proposition, even within the generation of self sufficient using, however OEMs can slender this hole by way of broadening the automobile’s price proposition thru augmented packages and linked products and services.

As soon as absolutely self sufficient using is conceivable – and that is now not a delusion since stage 3 approvals are already being bought by way of OEMs[1] – the car-smartphone hole will also be narrowed a lot additional. The important thing shall be to change into sessions which are these days spent purely on using/transportation into immersive visitor reports, and thereby increase the worth proposition so far as conceivable.

Present analysis within the box of self sufficient using basically specializes in its technical feasibility and enablement, and neglects the client’s position, and particularly that of the motive force. The growth against self sufficient using will step by step flip drivers into passengers. As that evolution occurs, the motive force’s consideration will also be transferred to different actions. Subsequently, the position of linked products and services will have to be reconsidered: They’re now not restricted to helping the motive force all the way through the adventure, however will be capable to deal with a much broader vary of spaces and functionalities, remodeling the automobile into an “revel in tool.”

Greater than 50% of our survey contributors state that after self sufficient using turns into conceivable, they wish to use leisure options (e.g. on-line video games, movies, tune), social media, and internet surfing options all the way through the time won. Those new alternatives don’t seem to be restricted to completely self sufficient using automobiles, however also are acceptable to initial levels reminiscent of freeway pilots or different stage 3 self sufficient using purposes.

OEMs must due to this fact rethink how other other people will use their merchandise. For the reason that drivers will develop into extra like passengers, and that buyers on the whole know precisely how they wish to use their spare time, nice alternatives for OEMs will emerge. Thus, we propose remodeling a adventure into an revel in the use of linked products and services.

This will also be completed by way of growing new packages in accordance with generation reminiscent of AR – as an example, video games the place you compete in opposition to different passengers and automobiles, or digital excursions thru towns and landscapes. Displayed content material is now not restricted to the on-board laptop or heads-up shows. Probably, all of the automobile can now be used for leisure and interplay. Treated this manner, the self sufficient automobile cannot simplest develop into a “lounge on wheels,” but additionally open up new trade alternatives within the car sector (e.g. growing workplaces or assembly rooms on wheels).

With this prolonged price proposition, OEMs can beef up their manufacturers with new provides and differentiating options available in the market.

Seamless integration

Some other hole recognized in our earlier article is that the automobile isn’t built-in right into a visitor’s virtual portfolio. These days, switching between other gadgets isn’t the versatile, seamless revel in that buyers be expecting and need. Our survey effects display the significance shoppers position on last this hole. For 42% of our contributors (57% in China), integration of smartphone apps into the automobile is a determinant of willingness to pay for linked products and services.

To meet this requirement, OEMs must now open up their ecosystems to third-party app builders. One of the simplest ways could also be for OEMs to determine an app retailer containing the total vary of (externally evolved) apps that buyers already use on their smartphones along its personal apps. Through together with those third-party apps, the client revel in is optimized because the transfer between smartphone, pill, and automobile is extra handy and seamless. This transfer to an open ecosystem has the additional benefit of providing OEMs new profit possible; one possibility is a revenue-share fashion the place a per-transaction fee is accrued – a an identical fashion to that utilized by the Apple App Retailer and Airbnb.[2] For the reason that automobile will then be perceived as an extra gross sales channel by way of exterior suppliers (e.g. Amazon), this will likely support the entire positioning of automobiles within the virtual portfolio.

To toughen and allow this seamlessness, centralized account control must be established, both inside the automobile or – much more with ease – by the use of the smartphone app related to the automobile. This option will allow shoppers to retailer the credentials had to log into the other app accounts as soon as after which routinely synchronize their other gadgets and app information with the automobile. Because of this, information consistency is ensured. Already, the most recent BMW fashions permit the consumer to log into their Spotify account by way of scanning a QR code.[3] Centralized account control would beef up ease of use even additional.

Ecosystem point of view: app availability & running machine

App availability

Somewhat few apps are to be had in linked automobiles when compared with the vast selection to be had to smartphone customers. Greater than part of survey contributors have 20-30 apps on their smartphones along with the pre-installed ones, and a few other people have much more.

Naturally, automobiles and telephones characteristic several types of apps: The most well liked ones at the smartphone have a tendency to narrate to social media, e-mail, messaging, and video games, while automobiles have a tendency to run apps reminiscent of navigation, infotainment and many others. On the other hand, that appears set to modify. Just about 60% of our contributors say they wish to have the similar number of apps of their automobiles as on their smartphones and would use them as intensively. This sense is most powerful in China, the place 82% choose that solution.

In line with the survey effects, greater than 65% of contributors would really like their automobiles to supply the similar navigation and tune or video streaming apps that they use on their telephones. Round 45% wish to have in-car get right of entry to to their smartphones’ information and social media apps; 35% would really like apps for cell banking, fee, e-mail, and charging electrical automobiles; and 33% for on-line buying groceries.

Consumers’ want to make use of smartphone apps of their automobiles reinforces our previous level that partnerships with 1/3 events shall be essential to good fortune in increasing the app panorama. So what kind of incentives and enablers must OEMs be offering to tempt builders into their ecosystem? Chances come with:

- Get entry to to information: As an example, an OEM may just be offering to toughen a web based supplier of restore and upkeep workshop products and services by way of sharing automobile standing knowledge to assist create personalised choices.

- Developer platforms to facilitate app building for the OEM’s levels: Mercedes-Benz /builders is an instance.

- Adoption of open-source insurance policies as same old to make it more straightforward for app builders to supply end-to-end toughen for apps in automobiles, from building to repairs and updates.

Centralization round a restricted selection of OSs

While the smartphone app marketplace is centralized round Google/Android and Apple/iOS, the car business’s OS panorama is a lot more fragmented, making it unattractive for third-party suppliers. We foresee that, as has already took place within the smartphone OS panorama, the car OS marketplace will develop into consolidated, regardless that to not moderately the similar extent. Extra insights referring to running programs and ecosystems are mentioned in Attached Automobile Pattern Radar 2.

In the meantime, particular person OEMs urgently wish to overview their OS technique. They’ve a collection of 3 choices:

- Use an present OS, most probably Android Automobile

- Construct their very own OS

- Take a hybrid means, the use of Android Automobile and the Android Open-Supply Venture (AOSP) as a place to begin and later development a complete OS panorama

In deciding between those choices, an OEM wishes to bear in mind a number of strategic questions. How smartly do same old answers have compatibility the trade’s wishes? What are the important thing drivers of the OS for patrons? (Top rate and quantity OEMs might solution that closing query in a different way.) And what kind of funds is to be had for OS building?

Whichever of the 3 choices an OEM selects, we propose pursuing it in collaboration with appropriate companions. OEMs must assume strategically about how absolute best to cooperate with different OEMs, IT corporations, and even corporations in different industries.

Collaborations between OEMs are already below dialogue. BMW, Daimler, and VW not too long ago introduced their goal to construct a not unusual OS for e-cars, regardless that they had been due to this fact not able to agree some way ahead. Such collaborations might take quite a lot of paperwork: As an example, an OEM with its personal OS may just license it to others as a provider. We strongly counsel that OEMs goal to check the top requirements of capability and reliability set by way of IT corporations to safeguard their competitiveness in the event that they make a decision to stay OS building inside the car business.

Actually, partnering with IT corporations, and capitalizing on their strengths within the OS house, is very important. Those corporations have now not been gradual to go into the car business themselves. Google introduced Android Automobile in 2017, and by way of 2022 it’ll characteristic in additional than 15 automobile fashions, from manufacturers together with Polestar, Basic Motors, Ford, Renault, Nissan, and Stellantis. Seven years after the release of Apple CarPlay, Apple plans so as to add weather management, speedometer, and seat adjustment to CarPlay by the use of cooperation with OEMs. Sooner or later, Apple will perhaps additionally put into effect its CarPlay inventions in electrical automobiles of its personal.[4]

Era point of view: innovation & updatability

Building time

Cars have a for much longer building cycle than smartphones do. Vehicles generally take a minimum of 5 to 6 years to increase, when compared with one or two years for smartphones. Partially as a result of this lengthy cycle, a automobile can already appear out of date when it’s introduced.

OEMs have two major techniques to near this hole. The primary is to undertake customer-centric product building approaches, which is able to assist to make sure that visitor wishes are met by way of the completed product. Through involving the client as early as conceivable in building, and keeping up that discussion right through the improvement cycle, OEMs can higher perceive present necessities and ache issues, and expect long term ones.

The second one option to shut this hole is to deploy software-based or virtualized ways to additional accelerate building. One benefit of this means is that automobile designers and testers can check new automobiles ahead of they’re constructed by way of the use of digital answers reminiscent of AI-powered simulations, in conjunction with augmented and digital fact. This may cut back building time considerably and the consequent product may be higher as a result of extra configurations will also be evaluated and examined, with fewer bodily prototypes (this means that much less price). Some other benefit of software-based or virtualized ways is they make it conceivable for patrons to take a look at out the automobile’s consumer revel in all the way through the early levels of building. That manner, the shoppers can give early comments to automobile designers to tell building iteration. Ways like this are already being utilized by business leaders as they are able to cut back time-to-market; bodily checking out with shoppers will also be utterly disregarded generally.

Processing and reaction time

A automobile is extra restricted than a telephone as to the volume and form of information it may well paintings with, and the way it can use this knowledge. To bridge this hole, OEMs wish to change into these days’s hardware-defined automobiles into the next day to come’s software-defined ones.

Lately’s building means can’t toughen software-designed automobiles as a result of the best way utility is created. Even supposing OEMs construct some utility parts in-house or in shut collaboration with strategic companions, they purchase others in from quite a lot of providers, then combine them as absolute best they are able to. The result’s that the standard automobile depends on a variety of building languages and utility constructions, resulting in incompatibilities and inconsistencies that have a tendency to power up complexity.

This means is an increasing number of problematic since the “softwarization” of these days’s automobiles calls for seamless integration of subsystems and parts. OEMs due to this fact wish to put nice emphasis on decoupling their {hardware} building cycles from the ones for utility, so as to increase utility sooner and deploy it extra incessantly. They will have to additionally streamline the improvement means, and align building languages and utility structure, irrespective of who’s growing each and every part. OEMs must additionally take into consideration their talent to procedure and analyze information successfully; the proliferation of packages and sensors in automobiles will quickly create a “information explosion” for which OEMs wish to get ready if they’re to reach a sufficient reaction time.

If finished as it should be, offloading heavy processing to the cloud is otherwise to enhance the responsiveness of linked products and services. OEMs must due to this fact paintings with their companions to create a cloud-based virtual infrastructure that gives a wise, scalable basis for handing over linked reports to shoppers.

A few of these adjustments are already beginning to occur, as a part of a shift within the car business’s rationale. Fairly than including computer systems to automobiles, OEMs will sooner or later construct automobiles round computer systems.

Buyer point of view: usability & visitor interplay

- Re-design the linked products and services portfolio from a driver-centered revel in against a passenger-centered one – particularly for (semi-)self sufficient automobiles

- Combine recurrently used third-party apps and foster seamless synchronization throughout different gadgets by the use of centralized account control

Ecosystem point of view: app availability & running machine

- Perceive the sensible automobile as a component in shoppers’ virtual portfolio and make sure that they are able to use the similar virtual products and services (apps) within the automobile as on different gadgets.

- Act right away and believe strategic cooperation with different OEMs or large tech corporations to stick related if the OS turns into a choice criterion for automobile acquire.

Era point of view: innovation & updatability

- Undertake customer-centric product building approaches to higher perceive and combine these days’s and the next day to come’s marketplace necessities. Deploy software-based or virtualized ways to reveal shoppers to the automobile’s consumer revel in all the way through the early levels of building.

- Develop into these days’s hardware-defined automobiles into software-defined ones by way of decoupling {hardware} from utility building cycles. Construct a cloud-based virtual infrastructure to deal successfully with the approaching information explosion in automobiles.

Whilst tackling the gaps between automobiles and smartphones, we must bear in mind that we’re coping with a transferring goal. If it takes two to 5 years to near an opening and we commence now, there’s a chance that once we get to 2025 the automobile shall be similar with a smartphone from 2022 somewhat than one from 2025. To meet up with smartphones, we wish to look forward to what long term telephones shall be like.

We may also wish to query whether or not the smartphone is truly the fashion we must be aiming for. Will have to we in all probability be in search of inspiration from different industries and applied sciences as an alternative, or as smartly? We’ll pursue this line of enquiry in our impending Attached Automobile Pattern Radar record.

Authors:

Contributing Authors:

Marc Pauli, Yue Ma, Simon Monske, Michael Röller, Katharina Schepp, Konstantin Hauser and Christopher Hofmann

_______

[1] https://www.daimler.com/innovation/produktinnovation/autonomes-fahren/systemgenehmigung-fuer-hochautomatisiertes-fahren.html#:~:textual content=searchqueryp.c7Dp.c7Dp.c20p.cC3p.cBCbereinstimmen.-,Erstep.c20internationalp.c20gp.cC3p.cBCltigep.c20Systemgenehmigungp.c20fp.cC3p.cBCrp.c20hochautomatisiertesp.c20Fahren,einp.c20Levelp.c2D3p.c2DSystemp.cC2p.cB9

2 https://businessmodelnavigator.com/?identification=41

3 https://www.bmwusa.com/content material/dam/bmwusa/connected-drive/pdf/GSG_ConnectedMusic.pdf

[4] https://www.aroged.com/2021/10/08/bloomberg-apple-plans-to-add-climate-control-speedometer-and-seat-adjustment-to-carplay/

[5] https://international.chinadaily.com.cn/a/202110/23/WS61734c97a310cdd39bc70ba0.html